By Tayrê Balzan, Lucas Euzébio and Layon Lopes*

Direct Credit Society (SCD) and Peer-to-Peer Loan Company (SEP) are classified as credit fintechs, bringing technology and innovation to the traditional financial market and seeking to democratize credit. SCD and SEP also make it possible to offer credit to companies with more restricted access, proposing access to credit with less bureaucracy, speed in transactions, increased competition in the sector and a reduction in the cost of credit.

The financial sector is becoming increasingly modernized, largely due to the Banco Central do Brasil (BCB) acceptance of new technologies. Fintechs aim to democratize the financial sector by offering users credit services, but they still represent a small slice of the market. That’s why this article will look at the credit fintech market in Brazil.

What are credit fintechs?

Credit fintechs are companies that offer financial credit services 100% digitally, they don’t have any physical branches, avoiding the bureaucracy of traditional banks and offering more attractive interest rates. In BCB 2021 Financial Citizenship Report, it defined credit fintechs as important instruments in implementing financial inclusion policies, increasing efficiency and competition in the country’s credit market.

How are credit fintechs structured in Brazil?

A credit fintech in Brazil can be structured as a Direct Credit Society (SCD) or a People-to-People Loan Company (SEP), both of which are regulated by CMN Resolution No. 5,050/2022 and BCB CMN Resolution No. 4,656/2018.

SCD is a financial institution whose purpose is to carry out loan, financing and credit rights acquisition transactions exclusively through an electronic platform, using financial resources whose sole origin is its own capital. In addition, it can only provide the following services: credit analysis for third parties; collection of credit from third parties; acting as an insurance representative in the distribution of insurance related to its operations; issuing electronic money; issuing post-paid payment instruments (credit cards); acting as a payment transaction initiator.

SEP, on the other hand, is a financial institution whose purpose is to carry out lending and financing operations between people exclusively through an electronic platform. SEP carries out credit operations known as peer-to-peer lending, acting as a financial intermediary. In addition, it can only provide the following services: credit analysis for clients and third parties; collection of credit from clients and third parties; acting as an insurance representative in the distribution of insurance related to its operations; issuing electronic money; and acting as a payment transaction initiator.

Article 22 of CMN Resolution 5.050/2022 states that SEP is prohibited from carrying out loan and financing operations with its own resources, participating in the capital of financial institutions, co-obliging or providing any type of guarantee in loan and financing operations, remunerating or using for its own benefit the resources relating to loan and financing operations, transferring funds to debtors before they are made available by creditors, transferring funds to creditors before they are paid by debtors, keeping creditors’ and debtors’ funds in an account they own that is not linked to the loan and financing operations and linking the completion of the credit operation to the efforts of third parties or the debtor, as an entrepreneur.

Based on the definitions of SCD and SEP, it can be seen that the main difference between them is that SEP cannot use its own resources for loan and financing operations, but must use the resources made available by creditors to carry out the operations.

How is the credit fintech market doing in Brazil?

The credit fintech market in Brazil has grown considerably. According to the list of institutions authorized, regulated or supervised by the BCB surveyed in September 2023, 112 SCDs and 12 SEPs had already been authorized to operate by BCB.

Alson, according to the 2021 Financial Citizenship Report, the document showed that credit fintechs mostly served legal entities. The SCDs granted a total of approximately R$2.7 billion in credit to legal entities, and R$931 million to individuals. SEPs, on the other hand, granted a total of approximately R$ 172 million in credit to legal entities and R$ 13 million to individuals.

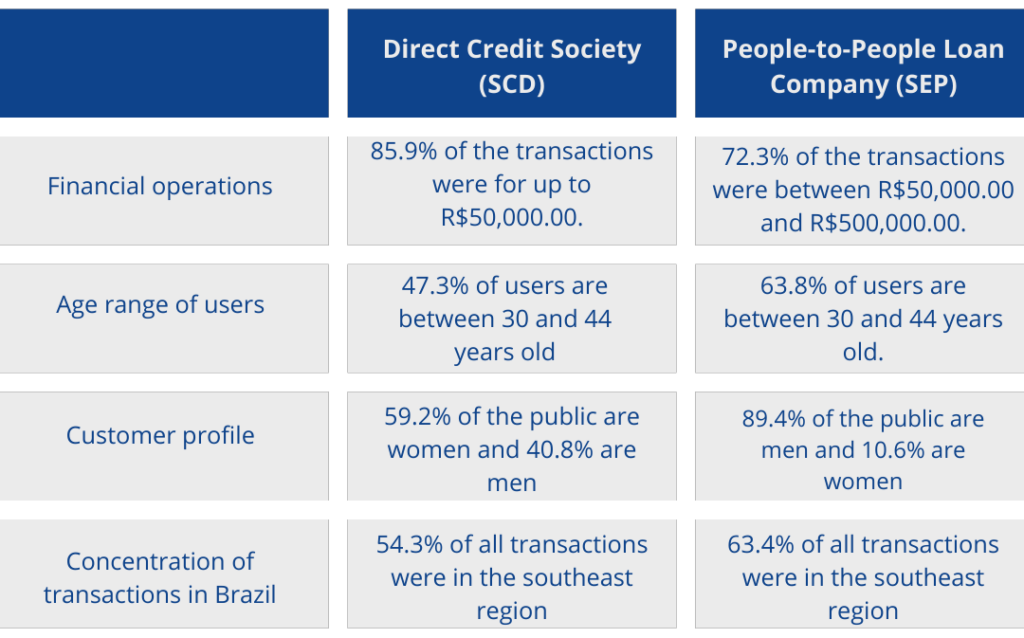

Other relevant data presented in the report on the credit fintech market in Brazil, especially regarding natural persons:

From the data reported above, one can see the relevance of the study for credit fintechs in Brazil, especially to understand: (i) where the market is concentrated; (ii) the characteristics of the client; and (iii) how the product will be presented in the market.

Although the credit fintech market in Brazil is growing annually, it still represents a small portion of the financial market, with an estimated representation of only 5% of the total volume of operations.

In addition, Brazil has approximately 34 million people who do not have a bank account, which makes the credit fintech market even more attractive, making it possible to serve this fraction of the population by granting credit that, in a traditional bank, would not be possible due to excessive bureaucracy.

If you are interested in entering the credit fintech market in Brazil, it is essential that you consult specialized legal advice to help you build your journey.

Have any questions? The team at Silva Lopes Advogados can help!

*Layon Lopes is the CEO of Silva | Lopes, Euzébio is a partner and Tayrê Balzan is a member of the Silva | Lopes team.